Understanding financial terms can sometimes feel overwhelming, especially when you're navigating the world of banking. One of the most common questions people ask is whether an ABA number and a routing number are the same. The answer is yes—both terms refer to the same nine-digit code used to identify financial institutions in the United States. This article will explore the concept in detail, ensuring you're well-equipped with the knowledge you need to manage your finances effectively.

In today's digital age, where online banking and transactions are becoming increasingly prevalent, understanding the nuances of banking terms is essential. ABA numbers and routing numbers play a crucial role in ensuring that your money reaches the right destination during transfers. Whether you're setting up direct deposits, paying bills, or transferring funds internationally, knowing how these numbers work is vital.

Throughout this article, we will delve into the specifics of ABA and routing numbers, their functions, and how they impact your banking activities. By the end of this piece, you'll have a clear understanding of whether these terms are interchangeable and how to use them effectively.

Read also:Erie Insurance Rental Car Comprehensive Guide To Coverage Benefits And Faqs

Table of Contents

- What is an ABA Number?

- Is ABA Number and Routing Number the Same?

- Functions of ABA/Routing Numbers

- How to Find Your ABA/Routing Number

- Types of Routing Numbers

- Security Concerns with ABA/Routing Numbers

- ABA Numbers in International Transactions

- The History of ABA Numbers

- Frequently Asked Questions

- Conclusion

What is an ABA Number?

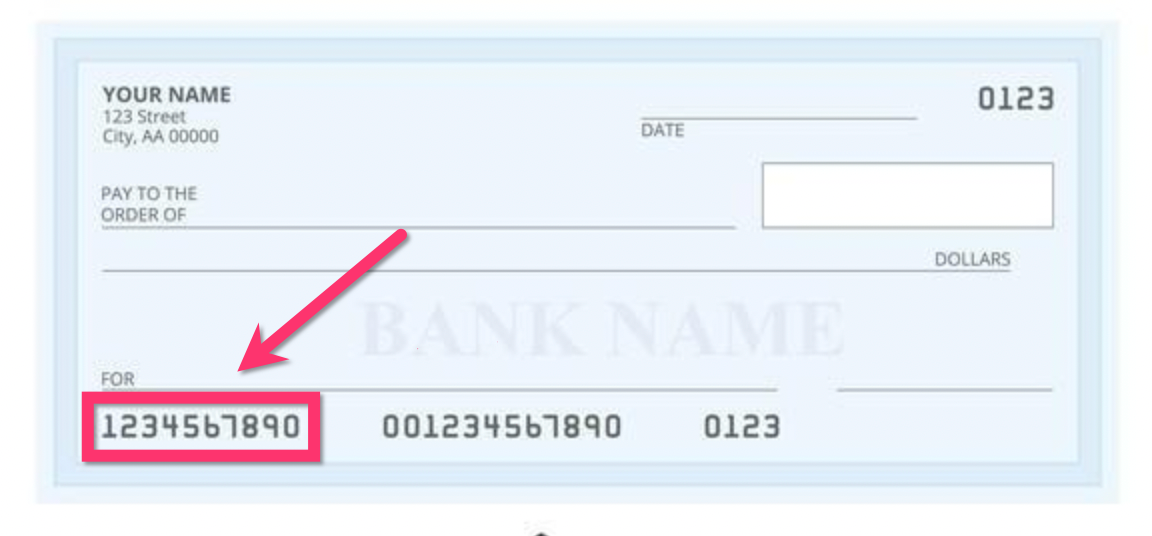

An ABA number, or American Bankers Association number, is a unique nine-digit code assigned to financial institutions in the United States. It was first introduced in 1910 by the ABA to standardize the process of identifying banks and routing funds. This number is essential for various banking activities, including check processing, wire transfers, and electronic payments.

The ABA number is printed on the bottom left-hand corner of your checks, along with your account number and check number. Each digit in the ABA number has a specific purpose, ensuring accuracy and security in financial transactions.

Structure of an ABA Number

- First four digits: Represent the Federal Reserve Routing Symbol.

- Next four digits: Identify the specific bank or financial institution.

- Last digit: Acts as a check digit to verify the accuracy of the number.

Is ABA Number and Routing Number the Same?

Yes, an ABA number and a routing number are the same. The terms are used interchangeably in the banking industry. Both refer to the nine-digit code that helps identify your bank and ensures that your money is routed to the correct financial institution during transactions.

This number is crucial for domestic transactions within the United States. Whether you're setting up direct deposits, paying bills online, or transferring funds between accounts, the ABA/routing number ensures that the transaction is processed accurately and efficiently.

Why the Confusion?

The confusion often arises because different banks and financial institutions may use different terminology. Some may refer to it as an ABA number, while others may call it a routing number. Regardless of the term used, the function and purpose remain the same.

Functions of ABA/Routing Numbers

The primary function of an ABA/routing number is to facilitate the routing of financial transactions between banks. Here are some of the key functions:

Read also:Does Brighton Allow Snowboarders A Comprehensive Guide

- Check Processing: When you write a check, the ABA number ensures that the funds are drawn from the correct account at the correct bank.

- Wire Transfers: ABA numbers are used to route funds during domestic wire transfers.

- Direct Deposits: Employers use ABA numbers to deposit salaries directly into employees' accounts.

- Automated Clearing House (ACH) Transactions: ABA numbers are essential for processing electronic payments and transfers.

How to Find Your ABA/Routing Number

Locating your ABA/routing number is relatively straightforward. Here are some common methods:

On Your Checks

As mentioned earlier, the ABA number is printed on the bottom left-hand corner of your checks. It is the first set of numbers in the string of codes at the bottom of the check.

Online Banking

Most banks provide your ABA/routing number in the online banking portal. You can usually find it under the account details or settings section.

Bank's Website

Many banks list their ABA/routing numbers on their official websites. Simply visit the bank's website and search for the routing number for your specific branch or account type.

Customer Service

If you're unable to locate your ABA number through the above methods, you can always contact your bank's customer service for assistance. They will be able to provide you with the correct number.

Types of Routing Numbers

While the basic structure of an ABA/routing number remains the same, there are different types of routing numbers based on the type of transaction:

Wire Routing Numbers

Wire routing numbers are used specifically for wire transfers. These numbers may differ from the ACH routing numbers used for electronic payments.

ACH Routing Numbers

ACH routing numbers are used for electronic payments and transfers, such as direct deposits and bill payments.

International Routing Numbers

For international transactions, banks may use a different set of numbers, such as SWIFT codes, to facilitate cross-border transfers.

Security Concerns with ABA/Routing Numbers

While ABA/routing numbers are essential for banking transactions, they can also pose security risks if they fall into the wrong hands. Fraudsters can use this information to initiate unauthorized transactions or gain access to your account.

To protect yourself, it's important to keep your ABA/routing number confidential and only share it with trusted entities. Most banks also offer additional security measures, such as two-factor authentication, to safeguard your account information.

ABA Numbers in International Transactions

While ABA numbers are primarily used for domestic transactions within the United States, they can also play a role in international transactions. However, for cross-border transfers, banks typically use SWIFT codes instead of ABA numbers.

SWIFT codes are unique identifiers assigned to banks worldwide and are used to facilitate international wire transfers. If you need to send money overseas, your bank may require both your ABA number and a SWIFT code to ensure the transaction is processed correctly.

The History of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Bankers Association introduced them to standardize the process of identifying banks and routing funds. At the time, the banking industry was growing rapidly, and there was a need for a standardized system to ensure accurate and efficient transactions.

Over the years, the ABA number system has evolved to accommodate advancements in technology and changes in the banking landscape. Today, ABA numbers remain a critical component of the financial infrastructure in the United States.

Frequently Asked Questions

Q: Can I use my ABA number for international transactions?

A: While ABA numbers can sometimes be used for international transactions, they are primarily intended for domestic use within the United States. For cross-border transfers, banks typically use SWIFT codes.

Q: Is it safe to share my ABA number?

A: It's generally safe to share your ABA number with trusted entities, such as your employer for direct deposits or utility companies for bill payments. However, you should avoid sharing it with unknown parties to protect your account information.

Q: Can I have multiple ABA numbers for the same bank?

A: Yes, it's possible to have multiple ABA numbers for the same bank, depending on the type of transaction and the location of the branch. For example, wire transfers and ACH transactions may require different routing numbers.

Conclusion

In conclusion, the terms ABA number and routing number are indeed the same, referring to the nine-digit code used to identify financial institutions in the United States. Understanding their functions and how to locate them is essential for managing your finances effectively.

By following the guidelines outlined in this article, you can ensure that your banking transactions are processed accurately and securely. Remember to keep your ABA number confidential and only share it with trusted entities.

We invite you to share your thoughts and experiences in the comments section below. If you found this article helpful, please consider sharing it with others who may benefit from the information. For more insights into banking and finance, explore our other articles on the website.